The inaugural Wealth Index Report by digital wealth coach Franc shows that South Africans earning over R30,000 a month are facing significant hurdles with saving enough and setting money aside for emergencies.

And when looking at those who earn even more—over R60,000 a month—the pressure and anxiety of handling larger sums of money become key issues.

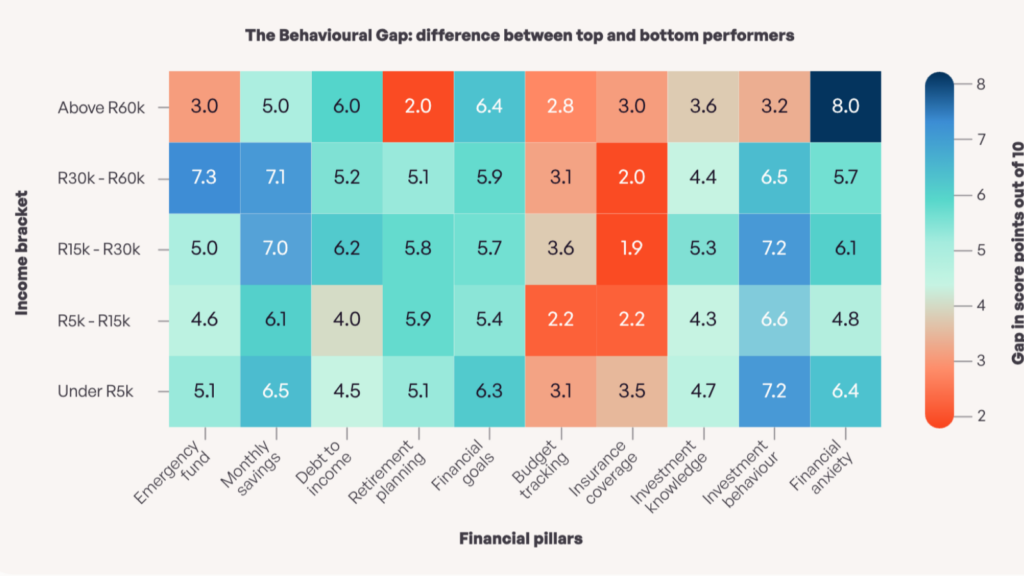

The data presented in the report lay out the biggest gaps, or “differentiators,” between the top and bottom performers in each income bracket in the study.

A large gap indicates significant inconsistencies among salary earners, suggesting struggles in managing that financial indicator. Smaller gaps point to the opposite.

For example, top earners show a very small differentiator gap in retirement planning, having ample resources available to structure their retirements adequately.

Lower earners, meanwhile, show larger gaps in investing and saving, with more limited funds available.

Although people on lower incomes struggle the most with investing and saving, those in the R30,000 to R60,000 bracket—considered high earners—show the same gaps.

The top performers in this bracket have generally built a cash buffer covering three months or more of expenses, Franc noted.

However, the underperformers often have no emergency savings, even though they earn above-average salaries.

In layman’s terms, the data shows that, while earners in this bracket have access to more funds, there is a significant gap between those who know how to handle it and those who do not.

This is in stark contrast to the highest bracket covered by the survey (R60,000+ a month), where the gap for emergency savings narrows significantly.

Among the top bracket, though, the highest earners experience financial anxiety and a negative mindset, rather than a lack of knowledge about saving.

In this bracket, the gap between the top and bottom performers is the largest overall, with an 8-point gap in financial anxiety.

Based on the report, the underperformers in this bracket often experience extreme stress and low confidence, while the top performers are referred to as “calm and confident.”

“At higher incomes, mindset is the differentiator. At the highest income levels, the differentiator is no

longer knowing how to save or how to invest, it is financial anxiety and mindset,” said Franc co-founder and CEO Thomas Brennan.

“High-income under-performers often report extreme stress and low confidence, whereas top performers at this level are calm and confident.”

Brennan said that this suggests that at high incomes, the struggle is often lifestyle inflation and the psychological pressure of managing larger sums.

South Africans aren’t prepared for emergencies

While there are significant gaps in emergency savings for higher earners, the report points to big problems in this indicator across most income groups.

Out of 3,952 respondents, 87% do not have enough emergency savings, which is less than three months’ income that has been set aside.

More than two-thirds of the South Africans surveyed (68.2%) cannot survive a one-month emergency.

One in four people is unable to save any money every month, and 70% of respondents are not adequately prepared for retirement.

Of the 70%, 38% do not have a sufficient plan in place for retirement, or have no retirement plan at all.

The report found that 78% of respondents had financial goals; however, more than half had no concrete plan to achieve them.

It was also revealed that 34% of respondents carry high debt burdens, with debt accounting for more than 35% of their income.

Among the survey respondents, it is clear that South Africans are not financially illiterate.

“64% rate their investment knowledge as intermediate or above. They are also not indifferent – most have goals and track their budgets at least monthly,” the group said.

However, a common theme in the report is that there is a key difference between knowing and doing, it added.

When predicting a high Wealth Index score, specific behaviours—such as investing regularly, budgeting consistently, and setting and reviewing financial goals—are significantly more effective than demographic factors like age, income, and education.

Individuals with strong financial habits also have two to three times higher odds of achieving a high Wealth Index score compared to those who simply have a higher income.

The report highlights two behaviours in particular, which hinder financial stability and the creation of wealth.

“Carrying high debt doesn’t just drag down your debt score, it significantly worsens saving and investment behaviour, financial anxiety and emergency preparedness,” the group said.

At the same time, having no emergency savings makes one considerably less likely to invest and adds to feelings of anxiety about money.