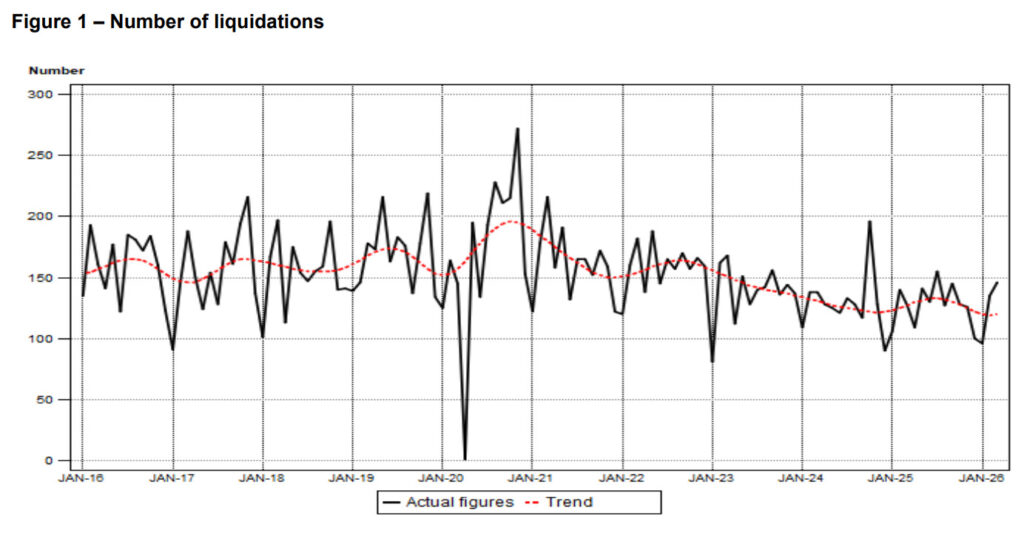

Liquidations in South Africa saw another sharp spike in March, rising 8% month-on-month, following a 40% surge in February.

According to the latest liquidation statistics from Stats SA, the country recorded 146 liquidations in March 2026, up from 135 the month before.

When added to the 96 recorded in January, the country experienced 377 liquidations in the first quarter.

Year-on-year, liquidations were up a staggering 15% from March 2025, while the year-to-date figures (Jan-March 2026) have also climbed 1.1% y/y, bucking recent trends.

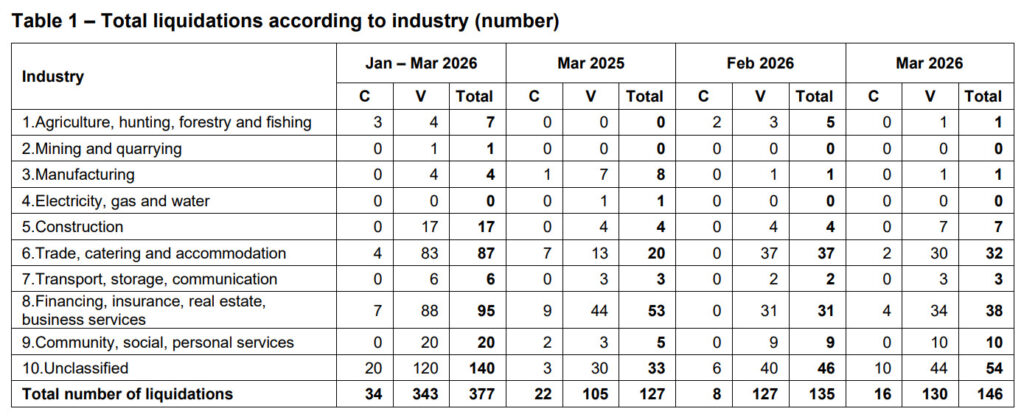

Most liquidations for the month were recorded in the finance, insurance, real estate, and business services sector, followed closely by the trade, catering and accommodation sector.

It should be noted that the liquidation data published by Stats SA is nuanced and only serves as one data point.

Specifically, liquidation doesn’t necessarily result from insolvency or operational difficulty—businesses can be liquidated voluntarily for transactional purposes.

The vast majority of liquidations tracked by Stats SA (circa 85%) are voluntary liquidations, initiated by the operations themselves.

While these might be related to solvency issues, this is not something the Stats SA data explicitly tracks.

A more important measure to track in a troubled business environment is compulsory liquidation, which is often a court-ordered process initiated by shareholders, creditors, or other stakeholders.

These are more directly tied to solvency and operational issues.

For March 2026, voluntary liquidations were much higher year-on-year (130 in March 2026 vs 105 in March 2025), with only 16 being compulsory (compared to 22 a year ago).

Compulsory liquidations for the first quarter are lower than in 2025, which could signal a better environment for businesses at the start of the year.

This generally aligns with most economic data for the period, reflecting improved sentiment in the country in January and February.

However, the m/m spike in compulsory liquidations in March, along with the overall upward trend, could also point to troubled waters for businesses in the wake of the war in Iran, which erupted at the end of February.

Businesses are taking a beating

The price pressure resulting from the war is already being felt by businesses and industries, with input and production costs spiking.

This is not only tied to the higher energy costs arising from global oil prices shooting past $100 a barrel, but also due to shocks along logistics and supply chains.

Headline producer price inflation (PPI) for March increased by 1.1% month-on-month, translating to 2.3% when measured on a year-on-year basis.

According to Investec economist Lara Hodes, this result was ahead of Bloomberg’s consensus expectations of 2.0% y/y.

The coke, petroleum, chemical, rubber and plastic products grouping added 0.4% to the monthly outcome on the back of a 20c/litre increase in the petrol price and over 60c/litre lift in the diesel price in March.

However, she stressed that these moderate price increases were based on oil prices and exchange rates prior to the onset of the war.

“More substantial inflationary pressure is expected going forward,” she warned.

Notably, April experienced a severe fuel price shock, with petrol prices rising by R3 per litre and diesel by R7 per litre. This was with the government’s R3 per litre fuel tax relief.

This is expected to have a significant impact on CPI and PPI for April.

Independent economist Elize Kruger and industry bodies previously warned that businesses will be feeling the pain over the near term at the very least, with an extended Iran War leading to more strain down the line.