The South African rand has weakened significantly since the onset of the war in the Middle East and is now ranked among the worst-performing emerging-market currencies.

According to Investec Chief Economist, Annabel Bishop, the rand is 3.5% weaker against the US dollar than before the war in the Middle East, while the US dollar is up 0.7% in comparison.

The rand was trading at R16.34 to the dollar, R22.10 to the pound and R19.23 to the Euro by 16h20.

Overall, the trade-weighted rand is 2.6% weaker, as the domestic currency has been negatively impacted, she said.

“Foreigners have sold R34.1 billion worth of South African bonds, weakening the rand to the third-worst performing emerging market currency in the Bloomberg ranking to date since before the Middle East war started,” she said in a Monday (20 April) note.

The rand is typically sold in risk-off periods.

Bishop said that, while the rand has pulled back from its weak point at the end of March, when it was 5.9% weaker than the US dollar, negative sentiment toward South Africa persists.

This is because South Africa is once again being grouped with riskier emerging market currencies—a stark shift from the positive-sentiment grouping it had before the war.

In the index, the rand is now ranked at the bottom of 21 currencies, alongside the Philippine Peso, Thai Baht, South Korean Won, Hungarian Forint, and Mexican Peso.

“These currencies are also the worst-performing in the carry trade, with global financial markets experiencing a negative carry trade return for these exchange rates, influenced also by rand depreciation itself on the return,” Bishop said.

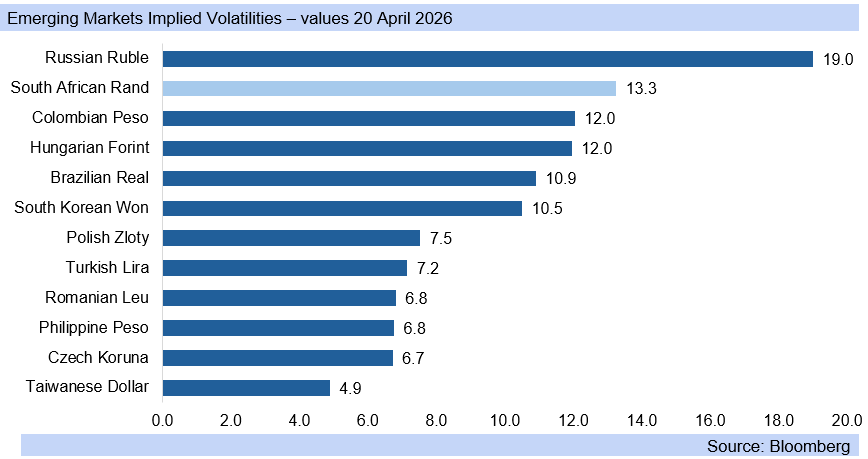

Among the currencies, the rand has experienced the greatest volatility, ranking among the most volatile emerging-market currencies. Its implied volatility is up significantly, the economist noted.

Warning signals ahead

Bishop flagged several risks lying ahead, even as the Middle East war continues to unwind slowly and unevenly.

The Brent crude oil is now priced around $95 a barrel, but futures are priced at only $82 a barrel by November.

This reflects a slow decline in spot prices, which is also evident in petrol and diesel futures, showing the same slow progress.

Analyses from Schroders and Bloomberg project similar outcomes, with optimistic scenarios pointing to $75 a barrel by the end of the year and downside scenarios exceeding $100 a barrel.

In both cases, prices are a far cry from the sub-$60-a-barrel levels seen before the war.

Also reflecting warnings from other analyses, Bishop noted that local fuel price recoveries are pointing to another massive increase in petrol and diesel prices for May.

While this is expected to be lower by month-end, it is unlikely to swing into positive territory (ie, a cut), while the question of the R3.00 per litre cut to fuel taxes being added back in remains uncertain.

Regardless, Bishop said the inflationary impact of the war so far is likely to only show up in April’s CPI figures, released in May.

This week’s publication of March’s CPI inflation figure is widely expected to be close to February’s 3.0% y/y, causing little rand impact.

Looking ahead, inflation is expected to rise, averaging 4% y/y for the second quarter.

“The war in Iran is only seen by financial markets currently to allow traffic in the Strait of Hormuz to return to normal by the end of June,” she said.

Bishop said the risk is to the upside for inflation from a longer war in the Middle East, which was expected to have ended by now.

“The risk, therefore, is for higher-than-expected inflation for South Africa, negatively affecting the rand,” she said.

This will ripple into decisions on interest rates, which are now expected to be hiked by 25 basis points at the Monetary Policy Committee’s May meeting.